One misconception about PCI DSS compliance in business is that the cost of compliance is high. The truth is that the cost of non-compliance is even higher than that. Whether it is PCI non-compliance fines, increased fees per transaction, or costs of breach cleanup and lawsuits by the customers, the financial cost is likely to get higher.

Compliance in PCI DSS for companies processing payments should be about minimizing risks, securing customer data, and maintaining customer trust. What happens when not pci dss compliant? Let us take a look at what happens when PCI DSS is non-compliant, the kinds of PCI DSS penalties involved, and why the cost of non-compliance may be more than the cost of compliance.

What does PCI DSS Non-Compliance mean?

The Payment Card Industry Data Security Standard (PCI DSS) provides a set of requirements for ensuring the security of cardholder data. All companies processing payment card information are supposed to be PCI DSS compliant no matter what their scale and specialization are.

Non-compliance takes place when businesses fail to satisfy the necessary controls, ignore the security assessment, or fail to properly secure payment environment. Note that even though PCI DSS doesn’t impose any fines, some other organizations can do it.

PCI DSS Penalties can add up quickly

One of the most immediate consequences of failing to comply is exposure to PCI DSS penalties. Depending on the severity and duration of non-compliance, acquiring banks may pass fines imposed by payment card brands directly to merchants.

Common financial penalties may include:

- Monthly fines until compliance is achieved

- Increased transaction processing fees

- Mandatory forensic investigations

- Costs associated with remediation efforts

- Potential suspension of card processing privileges

For organizations that rely heavily on credit card transactions, losing the ability to process payments can severely impact revenue streams. These PCI non-compliance fines penalties often become significantly more expensive than implementing compliance controls in the first place.

The cost of Data Breaches often exceeds compliance expenses

Many organizations only recognize the value of PCI DSS after experiencing a security incident. Unfortunately, by that point, financial damage has already occurred.

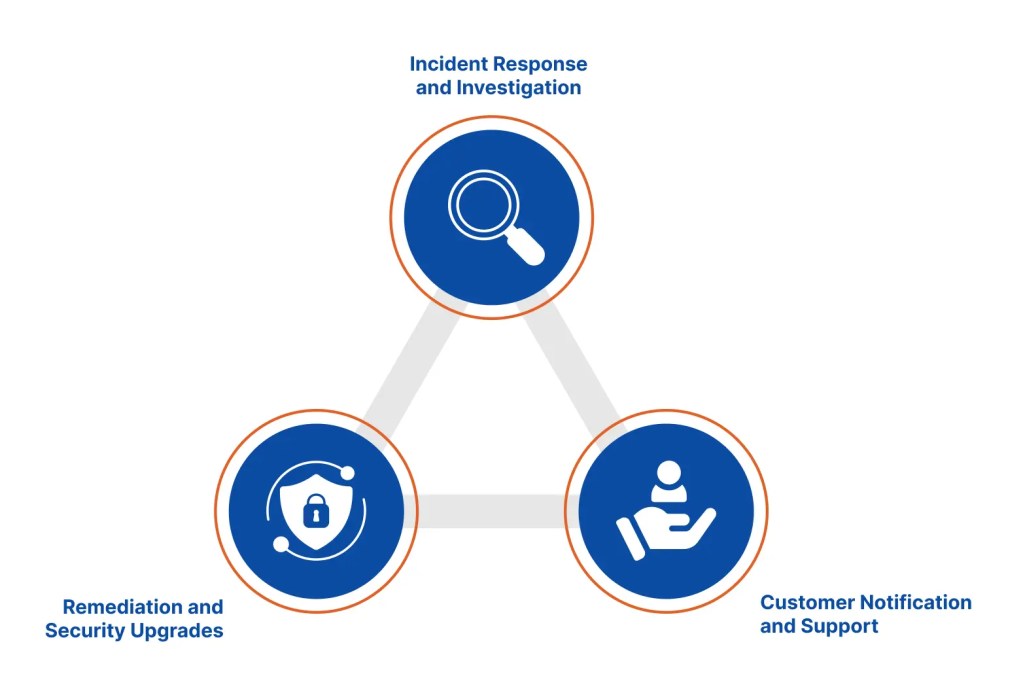

A payment card breach can trigger numerous expenses, including:

1. Incident Response and Investigation

Following a breach, organizations are typically required to conduct extensive forensic investigations to determine how attackers gained access and what data was compromised.

These investigations often involve:

- Digital forensic specialists

- Security consultants

- Legal advisors

- Regulatory reporting requirements

The costs can quickly escalate into tens or hundreds of thousands of dollars.

2. Customer Notification and Support

Many jurisdictions require affected customers to be informed when their sensitive information is exposed.

Businesses may need to provide:

- Notification letters

- Dedicated support teams

- Credit monitoring services

- Identity theft protection programs

These obligations significantly increase the overall cost of data breach recovery efforts.

3. Remediation and Security Upgrades

After a breach, organizations must strengthen security controls, implement additional monitoring, and often redesign vulnerable systems.

Ironically, companies frequently spend far more on post-breach remediation than they would have spent proactively achieving PCI DSS compliance.

Hidden operational costs of non-compliance

The financial consequences of non-compliance are not limited to fines and breach response costs. Many organizations face substantial operational disruptions that impact productivity and profitability.

1. Increased Audit Requirements

Businesses identified as non-compliant may be subject to more frequent audits and assessments. This creates additional administrative burdens and consumes valuable internal resources.

2. Business Downtime

Security incidents often force organizations to temporarily suspend payment processing systems while investigations and remediation efforts are underway.

The resulting downtime can lead to:

- Lost sales opportunities

- Delayed transactions

- Customer frustration

- Revenue loss

3. Higher Insurance Premiums

Cyber insurance providers increasingly evaluate security maturity when determining premiums and coverage terms. Organizations with poor compliance records may face higher costs or reduced coverage options.

Brand Damage is often the most expensive consequence

While financial penalties are measurable, reputational harm can be even more damaging.

Customers trust businesses to protect their sensitive payment information. When that trust is broken, rebuilding confidence becomes extremely difficult.

1. Loss of Customer Trust

Consumers are becoming increasingly aware of cybersecurity risks. A publicized breach may cause customers to:

- Avoid future transactions

- Move to competitors

- Leave negative reviews

- Share concerns across social media channels

Even long-standing customer relationships can be damaged by a single security incident.

2. Reduced Business Opportunities

Many enterprise customers and partners evaluate security practices before entering business relationships.

Organizations with a history of compliance failures may struggle to:

- Win new contracts

- Retain existing clients

- Pass vendor security reviews

- Meet procurement requirements

This can directly affect future growth and revenue potential.

3. Negative Media Coverage

Cybersecurity incidents frequently attract media attention. News coverage surrounding a payment card breach can amplify customer concerns and create lasting reputational challenges.

Unlike direct financial penalties, brand damage can continue affecting a business for years after the original incident.

Legal and Regulatory Exposure

Another often-overlooked consequence of PCI DSS non-compliance is legal liability.

When customer data is compromised, organizations may face:

- Class-action lawsuits

- Regulatory investigations

- Settlement costs

- Legal defense expenses

Depending on applicable privacy regulations, businesses could face additional penalties beyond standard PCI enforcement actions.

As data protection laws continue to evolve globally, organizations must recognize that non-compliance can create multiple layers of legal and financial risk.

What happens if Not PCI DSS compliant?

Organizations frequently ask, what happens if not pci dss compliant?

The answer varies depending on the circumstances, but common outcomes include:

- Financial penalties from payment card brands

- Increased processing fees

- Mandatory audits and assessments

- Data breach-related expenses

- Legal and regulatory scrutiny

- Customer attrition

- Reputational damage

- Potential loss of payment processing capabilities

In severe cases, the cumulative impact can threaten business continuity and long-term profitability.

Why does investing in compliance make business sense?

When evaluating compliance initiatives, organizations should view PCI DSS as a risk-reduction investment rather than a regulatory obligation.

Compliance helps organizations:

- Reduce breach likelihood

- Strengthening security controls

- Protect customer trust

- Minimize legal exposure

- Improve operational resilience

- Demonstrate commitment to data protection

Compared to the financial and reputational consequences of non-compliance, the investment required to maintain PCI DSS compliance is often relatively small.

Final Thoughts

In addition to the fine for non-compliance, there is an additional cost for not being PCI DSS compliant. Organizations that do not properly protect their cardholder information run into financial losses, operational challenges, legal issues, and reputational harm. The hidden costs of PCI DSS, ranging from the cost of PCI DSS fines to recovery costs, customer loss, and missed business opportunities, might add up and become much more expensive than compliance itself.

Organizations need to consider PCI DSS compliance as not only a necessity but also a strategic way to ensure business revenues, build customer confidence, and develop their business.

Protect your business from data breaches and avoid the cost of non-compliance and negative reputation impact. Whether you’re preparing for an assessment, addressing security gaps, or building a long-term compliance strategy, our experts at ValueMentor can help you reduce risk and protect cardholder data with confidence. Contact us to start your PCI DSS compliance journey.

FAQs:

PCI non-compliance fines are financial penalties that acquiring banks may impose on businesses that fail to meet PCI DSS requirements for protecting cardholder data.

2. Who can be fined for non-compliance with the PCI DSS standards?

All those businesses that store, process, and transmit payment card information may have to pay fines in case of non-compliance with the PCI DSS standards.

3. What will happen if there is a data breach by a non-compliant company?

There will be fines, forensic costs, legal costs, cost of notifying customers, and reputational damages.

4. Can PCI DSS non-compliance affect payment processing privileges?

Yes. In severe cases, businesses may face restrictions or even lose the ability to process payment card transactions.

5. Are PCI DSS penalties the same for every business?

No. Penalties vary based on factors such as the severity of non-compliance, breach impact, transaction volume, and acquiring bank policies.

6. How does being PCI DSS compliant help to reduce the cost of a data breach?

PCI DSS requires controls that decrease attack probability, thus allowing them to prevent breaches and save costs.

7. Can small businesses be fined for being non-compliant with PCI DSS?

Yes, as PCI DSS requirements concern all types of businesses working with payment card information.

8. Is PCI DSS compliance enough to protect an organization from cyberattacks?

No, although it considerably increases security, it still needs to be complemented by risk management activities.

9. How often should organizations assess their PCI DSS compliance status?

Organizations should review their compliance regularly and whenever significant changes are made to their payment environment.

10. What is the first step toward achieving PCI DSS compliance?

Conducting a scoping & gap assessment is often the best starting point, as it helps define PCI DSS scope and identify security weaknesses and compliance gaps that need to be addressed.