Payment card data drives the cashless economy. If mishandled, it can expose businesses to devastating breaches and regulatory penalties. The wrong selection of the Self-Assessment Questionnaire enhances the risk factor multiple times, keeping organizations in a false sense of security, or sometimes creating some unnecessary burden on teams, leading to wastage of various resources and time. This makes it extremely crucial to make the right selection of SAQ aligned with the payment environment. With a comprehensive understanding of questionnaire types, eligibility criteria, and by avoiding common selection pitfalls, businesses can move from compliance confusion to strategic security assurance. This blog acts as a guide in the process of making the right PCI DSS SAQ choice for your business.

What Exactly Is a PCI DSS SAQ and Why Does Your Business Need One?

The PCI DSS SAQ (the Payment Card Industry Data Security Standard Self-Assessment Questionnaire) is a compliance type designed for merchants and service providers who deal with card data operations, such as processing, storing, or transmitting cardholder data. Compared to a full-scale Level-1 audit, the SAQ enables organizations to perform a self-evaluation of their compliance position, considering the PCI DSS requirements. A standard set of technical and operational standards has been established to protect payment and card information.

There are various SAQ types specially designed for each requirement, specific merchant level, and processing environment. SAQ A, for example, is applicable for e-commerce merchants who are using third-party services for the cardholder data-related processing. SAQ D is more inclusive and covers all PCI DSS requirements; it is mostly assigned to larger merchants or those who have on-premises data storage. If there is a mistake in the SAQ type selection, then it can result in nullifying the effort and further leading to unnecessary scrutiny.

The importance of SAQ is not limited only to regulatory obligations. For payment processors and acquiring banks, PCI DSS is mandatory, PCI DSS is a mandatory requirement; it is even one of the crucial contractual requirements. Non-compliance can result in various kinds of financial penalties, increased transaction fees, or termination of merchant accounts. Failure to address PCI DSS controls, such as cardholder data encryption, secure network architecture, and access control mechanisms, provides attack surfaces to cyber attackers.

Let’s explore a real example: One data breach incident involving payment card data triggers forensic investigations, legal liabilities, and reputational damage. This can be way more compared to the cost of compliance. The SAQ serves as a structured framework to identify gaps before they become incidents.

Additionally, SAQs are not just static documents; they need to be completed annually and whenever a significant update to the cardholder data environment is made. These periodic assessments ensure that security controls evolve alongside infrastructure changes, vendor integration, and emerging threat vectors. For businesses handling payment data, the SAQ is a foundational aspect, considering functional resilience.

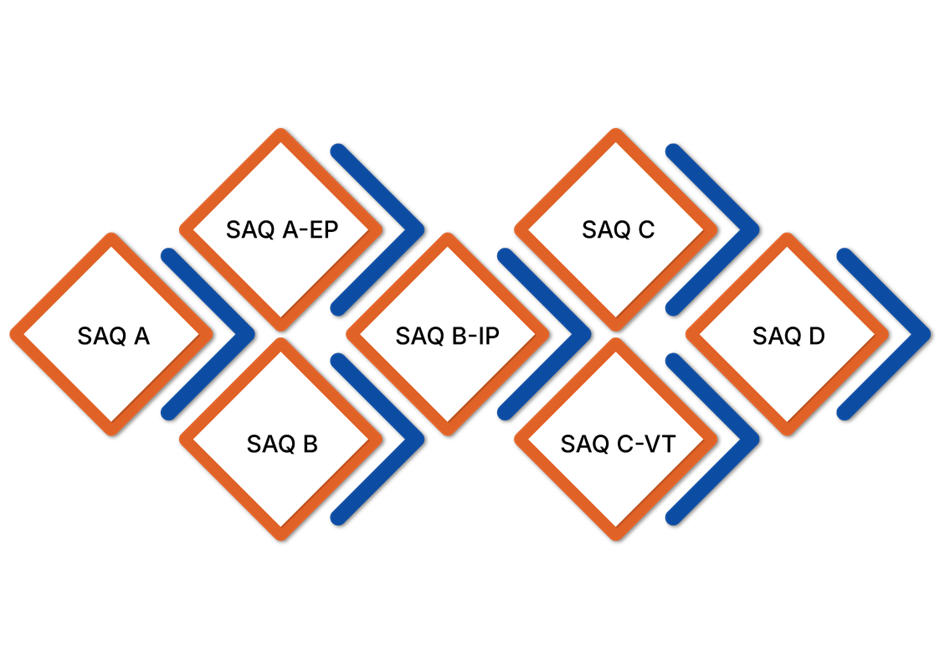

What Are the Different Types of SAQs and How Do They Differ?

The PCI Security Standards Council has developed nine distinct SAQ types based on all the different types of payment environments. Lack of understanding may potentially lead to leaving critical security gaps unaddressed.

- SAQ A: Is exclusively dedicated to card-not-present merchants and completely relies on outsourced payment processing. Their systems do not store, process, or transmit card data by any electronic means. All transactions are taken care of by the PCI DSS-compliant third-party providers. The fewest requirements, typically around 22 validation points, making it an option with the minimum burden.

- SAQ A-EP: This SAQ type is designed for e-commerce merchants using their website, and only the payment process is outsourced to a validated third party. These merchants have the payment page even though the cardholder data flows directly to a PCI DSS-compliant third party. This makes it essential to ensure website security, access controls, and vulnerability management.

- SAQ B: SAQ B focuses on merchants using standalone, dial-out terminals or a card imprint machine no electronic cardholder data storage. The key differentiator is the restricted network access beyond the terminal itself. Physical security and terminal management remain the primary focus rather than network segmentation.

- SAQ B-IP: Designed for merchants using IP-connected payment terminals, for example, those that are integrated with point-of-sale systems. The network connectivity is the additional part that is not covered under SAQ B. Validation of network segmentation, firewall configurations, and encryption protocols is required under this type.

- SAQ C: Includes merchants with payment application systems with internet connectivity, but no electronic cardholder data storage. This category demands rigorous attention to application security, including patching schedules, access logging, and secure authentication mechanisms.

- SAQ C-VT: applies to merchants who manually enter cardholder data via virtual terminal applications accessed through a web browser, with no electronic cardholder data storage. Human interaction with sensitive data elevates risk, necessitating controls around workstation security and access management.

- SAQ D: represents the most comprehensive assessment, applicable to all other merchant environments and service providers. It encompasses all 12 PCI DSS requirements and hundreds of validation points, often requiring significant technical documentation and evidence collection. SAQ-D is of two types, for merchants and service providers. If the entity is a service provider, the only applicable SAQ type is SAQ-D.

Each SAQ type reflects a distinct threat landscape shaped by how cardholder data flows through and potentially persists within the organization’s infrastructure.

How Do You Determine Which SAQ Type Applies to Your Business?

Determining the correct SAQ type requires a systematic technical audit of your payment infrastructure, not assumptions based on merchant category or revenue. Begin by conducting a comprehensive cardholder data flow analysis. Document for every point where payment information enters your environment, which systems process or transmit it, and where it exits or gets stored. This mapping exercise often reveals unexpected scope elements, backup systems retaining old transaction logs, development servers with production data copies, or firewall logs capturing unencrypted card details.

Next, assess your processing methodology with surgical precision. If your website collects payments, determine whether the payment form loads from your server or redirects entirely to a third-party payment processor. Even subtle implementation differences, such as using a payment provider JavaScript hosted on your domain versus a complete off-site redirection, fundamentally alter SAQ classification.

Examine your point-of-sale systems/terminals and standalone units with no network connectivity, IP-connected devices on your corporate network, or integrated systems sharing infrastructure with other business applications?

Critically evaluate data persistence. Many organizations believe they don’t store cardholder data, yet discover it exists in application logs, email archives, database backups, or error reporting systems. Electronic storage of any cardholder data, even temporarily, disqualifies you from simplified SAQ types regardless of your processing method.

Validate your findings through penetration testing or technical assessments that verify architectural assumptions match operational reality. Cross-reference your conclusions against official PCI Security Standards Council documentation rather than relying solely on payment processor recommendations, as vendors sometimes suggest SAQ types that benefit their operations rather than accurately reflecting your environment.

What Common Mistakes Should You Avoid When Selecting an SAQ?

The most prevalent error is assuming that business size or transaction volume dictates SAQ eligibility. In reality, technical architecture and data flow patterns determine the appropriate questionnaire type. A small business processing a million annually may qualify for SAQ A, while a lower-volume merchant with on-premises card storage requires SAQ D.

Another critical misstep involves overlooking system interconnections. Merchants often believe that outsourcing payment processing eliminates all compliance obligations. However, if your website hosts payment forms, even those managed by third-party JavaScript, you likely fall under SAQ A-EP rather than SAQ A. This distinction introduces dozens of additional requirements related to web application security and vulnerability management.

Another mistake is the failure to account for legacy systems represents another blind spot. Organizations frequently maintain outdated terminals, backup servers, or development environments that store cardholder data without proper decommissioning. These forgotten systems expand PCI DSS scope significantly, potentially disqualifying the business from simplified SAQ types entirely.

Relying solely on vendor assurances without independent verification also proves problematic. Payment processors may provide SAQ recommendations that serve their operational convenience rather than your actual compliance posture. Always cross-reference vendor guidance against official PCI SSC documentation and conduct internal technical validation.

Finally, treating SAQ selection as a one-time decision ignores the dynamic nature of IT environments. Infrastructure changes, new integrations, or modified payment workflows can invalidate your original classification, necessitating immediate reassessment rather than waiting for the annual compliance cycle.

Final Thoughts

PCI DSS SAQ compliance is not bureaucratic overhead. It is a structured defense against payment card breaches that destroy businesses. The questionnaire you select must mirror your actual technical environment, not aspirational simplicity or vendor convenience. Misclassification creates dangerous blind spots where attackers operate undetected. Approach SAQ selection with the same rigor applied to penetration testing or incident response planning. Annual reassessment, honest technical evaluation, and proactive gap remediation transform compliance from a checkbox exercise into operational resilience. The payment infrastructure demands accuracy. Connect with ValueMentor for any support required regarding PCI DSS SAQ.

FAQS

1. What happens if you fail your PCI DSS SAQ?

Failure leads to higher fees (0.05% to 0.15%), fines ($5,000 to $100,000), or merchant account termination through your acquiring bank. You must fix issues within 30 to 90 days. Repeated failure may force a QSA audit instead of self-assessment.

2. Can you outsource PCI DSS compliance?

No. Outsourcing reduces scope, but you stay responsible. You must verify that service providers hold valid PCI DSS compliance through annual AOC reviews. You remain liable for vendor risk and breaches.

3. How often must SAQs be submitted?

Submit at least once a year. Usually, within 90 days after the fiscal year-end. Major changes like new payment systems or infrastructure updates require earlier reassessment.

4. What is the role of a QSA?

QSAs, required for Level 1 merchants, review SAQ accuracy, identify hidden scope, and provide attestations. Costs range from $15,000 to $50,000.

5. How does network segmentation affect the SAQ scope?

Effective network segmentation isolates the cardholder data environment and lowers the SAQ scope. It must be tested annually to confirm isolation and prevent unauthorized access.

6. What documentation must support SAQs?

Maintain network and data flow diagrams, inventories, firewall rules, access logs, scan results, patch records, security policies, incident plans, and security training evidence.

7. Do PCI DSS requirements differ for e-commerce and retail businesses for e-commerce versus retail businesses?

E-commerce requires web app security, code reviews, scans, and TLS checks. Retail focuses on physical security and POS protection. Both protect cardholder data.

8. What is the difference between PCI DSS compliance and certification?

PCI DSS compliance means meeting requirements and validating annually. No formal “PCI DSS certification.” Compliance is ongoing.