PCI DSS compliance in the UAE is no longer just a regulatory checkbox it’s a business-critical priority for banks, fintechs, and payment providers operating in today’s fast-moving digital economy. With the rapid growth of contactless payments, mobile wallets, and cross-border transactions, the risk of cyber threats has increased significantly. Protecting cardholder data is essential not just for compliance, but for maintaining customer trust and business continuity.

Failing to meet PCI DSS requirements can expose organizations to:

- Data breaches and sensitive card data leaks

- Cyberattacks such as malware, phishing, and application-layer exploits

- Regulatory penalties from authorities like the Central Bank of the UAE

- Financial losses and fraud liability

- Damage to brand reputation and customer confidence

In this blog, we’ll walk you through:

- The evolving payments landscape in the UAE

- Key regulatory expectations from the Central Bank

- A simple, practical approach to achieving PCI DSS compliance

Whether you’re a CISO, compliance professional, or fintech founder, this guide will help you understand what’s required-and how to get there without unnecessary complexity.

UAE Payment Landscape & CBUAE Regulatory Overview

The UAE’s payment ecosystem is evolving rapidly, fueled by the growth of digital wallets, contactless payments, and fintech innovation. As the ecosystem expands, ensuring secure and reliable transactions has become a top priority.

The Central Bank of the UAE plays a key role in this transformation by setting regulatory expectations that focus on:

- Data security

- System resilience

- Fraud prevention

Financial institutions that handle card transactions are expected to align with global standards such as PCI DSS. While PCI DSS itself is not a law, it is enforced through regulatory frameworks, licensing conditions, and audit requirements set by the Central Bank.

In practice, this means: Compliance is essential to maintain operational licenses and non-compliance can lead to penalties, restrictions, or increased regulatory scrutiny.

Additionally, regulations covering:

- Stored Value Facilities (SVF)

- Payment Service Providers (PSPs)

- Open Finance frameworks

further strengthen the need for robust data protection and security controls aligned with PCI DSS. In a rapidly digitizing financial landscape, strong security is not just about compliance; it’s a competitive advantage that builds trust and enables sustainable growth.

PCI DSS applicability for UAE financial institutions

The level of PCI DSS applies to any organization that stores, processes, or transmits cardholder data regardless of size or transaction volume.

In the UAE, this means PCI DSS is relevant across a wide range of financial and payment ecosystem participants, including:

- Retail and commercial banks handling card issuance and payment processing

- Fintech startups offering payment solutions, wallets, or acquiring services

- Payment gateways and processors managing transaction routing and authorization

- E-commerce platforms that accept and process card payments online

In simple terms, if your organization is involved in card-based transactions at any stage, PCI DSS compliance is not optional it is a fundamental requirement for secure operations. Understanding whether PCI DSS applies to your organization is the first step toward building a secure, compliant, and scalable payment environment.

The level of compliance required depends on an organization’s transaction volume and its role in the payment ecosystem. Based on this, entities are categorized as merchants or service providers, each with specific validation requirements.

Depending on the classification, organizations may need to:

- Complete a Self-Assessment Questionnaire (SAQ)

- Undergo a formal audit by a Qualified Security Assessor (QSA)

- Obtain a Report on Compliance (ROC) for full validation (typically for higher-level merchants and service providers)

The Report on Compliance (ROC) is a detailed assessment report prepared by a QSA, confirming that all applicable PCI DSS requirements have been fully implemented and are operating effectively. Importantly, PCI DSS compliance is not limited to internal systems. For organizations in the UAE, it also extends to third-party service providers. Even if payment processing is outsourced, accountability cannot be transferred. As per PCI DSS expectations:

Organizations must ensure that all third-party vendors handling cardholder data are PCI DSS compliant and proper due diligence, continuous monitoring, and contractual controls must be in place. In short, outsourcing reduces operational effort but not compliance responsibility.

Key PCI DSS requirements for 2026

With PCI DSS v4.0, now fully enforced in 2026, organizations are expected to adopt a more flexible, risk-based approach while still meeting core security objectives to protect cardholder data.

1. Enhanced Access Control

- Organizations must implement strong identity and access management (IAM) practices to restrict access to sensitive systems

- Multi-factor authentication (MFA) is now mandatory for all access to the cardholder data environment (CDE)

- Access should follow the principle of least privilege

2. Continuous Monitoring and Testing

- Security is no longer periodic; it must be continuous and proactive

- Real-time monitoring and alerting mechanisms must be in place

- Regular vulnerability scans and penetration testing are required

- Organizations should be able to detect and respond to threats quickly

3. Strong Encryption Standards

- Sensitive cardholder data must be protected at all times

- Encryption is required for data in transit and at rest

- Only industry-approved cryptographic standards should be used

4. Secure Software Development

- For fintechs and digital platforms, secure development is critical

- Adopt secure coding practices

- Integrate security testing (SAST/DAST) into the development lifecycle

- Address vulnerabilities before production deployment

5. Customized Implementation Approach

- One of the biggest challenges in PCI DSS 4.0.1 is flexibility

- Organizations can design custom security controls based on their environment

- Controls must still meet the intent of PCI requirements

- Proper documentation and justification is mandatory

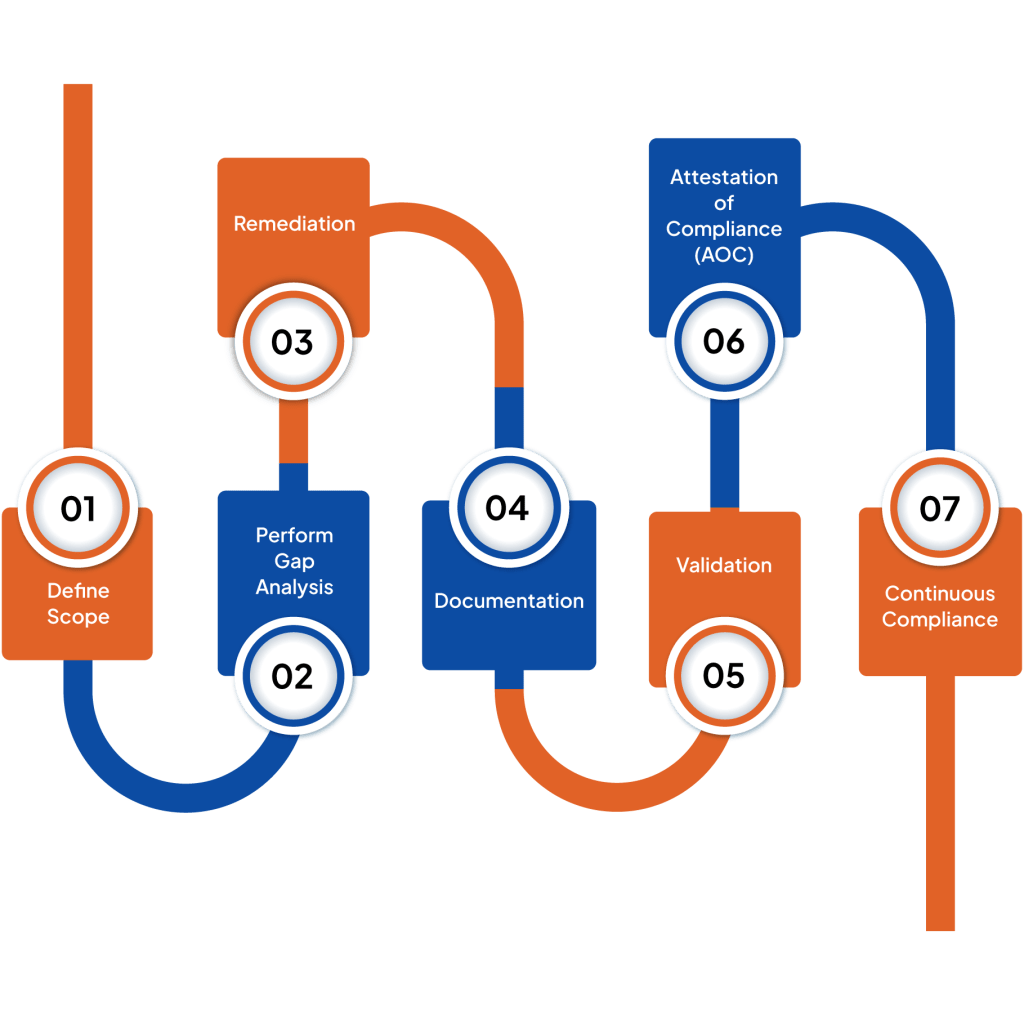

Step-by-Step certification path

Achieving PCI DSS compliance in the UAE requires a structured and practical approach. Here’s a step-by-step roadmap to guide your certification journey:

Step 1: Define Scope

Start by identifying all systems, people, and processes that interact with cardholder data. A well-defined scope helps:

- Reduce complexity

- Lower compliance costs

- Focus only on critical environments (CDE)

Step 2: Perform Gap Analysis

- Evaluate your current environment against PCI DSS requirements.

- Conduct an internal assessment or engage experts

- Identify gaps in controls, processes, and technologies

Step 3: Remediation

- Address the identified gaps by implementing required controls.

- Strengthen security configurations

- Deploy necessary tools (e.g., logging, encryption, monitoring)

- Align processes with PCI DSS expectations

Step 4: Documentation

- Prepare all required documentation to demonstrate compliance.

- Security policies and procedures

- System configurations and architecture diagrams

- Evidence to support control implementation

Strong documentation is essential for a smooth audit process.

Step 5: Validation

Validate your compliance based on your PCI level:

- Complete a Self-Assessment Questionnaire (SAQ) (for lower-level merchants), or

- Undergo an audit by a Qualified Security Assessor (QSA)

For organizations requiring full assessment, this process results in a Report on Compliance (ROC) in a detailed report confirming that all PCI DSS requirements are implemented and operating effectively.

Step 6: Attestation of Compliance (AOC)

Submit your compliance results, including the Attestation of Compliance (AOC) (and ROC, where applicable), to acquiring banks or regulators as required.

Step 7: Continuous Compliance

PCI DSS is not a one-time effort it’s an ongoing commitment.

- Continuously monitor systems

- Perform regular testing and reviews

- Update controls as threats evolve

Choosing a QSA with UAE Experience

Selecting the right Qualified Security Assessor (QSA) is a critical step in ensuring a smooth and successful PCI DSS certification journey.

For organizations in the UAE, it’s important to choose a QSA who not only understands PCI DSS requirements but also has strong familiarity with local regulatory expectations set by the Central Bank of the UAE.

A QSA with regional experience can:

- Align PCI DSS controls with UAE regulatory guidelines

- Provide insights into common audit observations and pitfalls specific to the UAE market

- Help streamline communication with regulators and acquiring banks

- Offer practical guidance based on real-world implementation experience

This localized expertise helps: Reduce certification delays, avoid rework during audits, ensure a more efficient and predictable compliance journey.

Common Challenges and Solutions

While PCI DSS compliance is essential, organizations often face practical challenges during implementation. Here are some common issues and how to address them effectively:

Challenge 1: Complex IT Environment

Many banks and fintechs in the UAE operate in hybrid environments (on-premise + cloud), which can make compliance more complex.

Solution: Use network segmentation to isolate the cardholder data environment (CDE) and implement tokenization to reduce the scope of sensitive data. This minimizes exposure and simplifies compliance efforts.

Challenge 2: Third-Party Risks

Reliance on third-party vendors and service providers can introduce additional risk.

Solution: Perform thorough due diligence and ensure all vendors handling cardholder data are PCI DSS compliant. Establish strong contracts, monitoring, and accountability mechanisms.

Challenge 3: Resource Challenges

Many fintechs and growing organizations may lack the dedicated resources or expertise required for compliance.

Solution: Leverage managed security services and automation tools to reduce operational burden. This helps maintain compliance without requiring large in-house teams.

Challenge 4: Keeping Up with Updates

New requirements in PCI DSS 4.0.1 can be complex and sometimes difficult to interpret.

Solution: Invest in regular training and collaborate with experienced QSAs. Staying informed ensures smooth adoption of new requirements and avoids audit surprises.

Cost Considerations for UAE Organizations

The cost of achieving PCI DSS compliance can vary significantly based on an organization’s size, complexity, and scope. While the investment may seem substantial, it plays a critical role in reducing long-term security and business risks.

Key Cost Factors

Organizations should typically account for:

Gap assessment and consulting fees Initial evaluation to identify compliance gaps and define a remediation roadmap

Technology investments Implementation or upgrade of security controls such as:

- Firewalls

- Encryption solutions

- Monitoring and logging systems

QSA audit costs Fees associated with engaging a Qualified Security Assessor (QSA) for validation and certification (including ROC, where applicable)

Ongoing compliance maintenance Continuous monitoring, periodic testing, training, and updates to maintain compliance

UAE-Specific Considerations

For organizations operating in the UAE, additional factors may influence cost, including:

- Alignment with local regulatory expectations from the Central Bank of the UAE

- Integration with regional payment systems and frameworks

- Localization and compliance reporting requirements

Is It Worth the Investment? Absolutely. The cost of compliance is often significantly lower than the cost of non-compliance, which can include:

- Data breaches and fraud losses

- Regulatory penalties

- Business disruption

- Long-term reputational damage

Key Takeaway

PCI DSS compliance should be viewed not as a cost but as a strategic investment in security, trust, and business resilience.

Conclusion

PCI DSS v4.0.1 compliance has become a critical priority for financial organizations in the UAE. With the rapid rise of digital payments and increasingly sophisticated cyber threats, banks and fintechs must take a proactive approach to securing cardholder data.

Aligning with PCI DSS requirements alongside regulatory expectations from the Central Bank of the UAE not only ensures compliance but also helps build customer trust, operational resilience, andlong-term business credibility.

By:

- Understanding PCI DSS requirements

- Following a structured certification approach

- Addressing common challenges proactively

- Organizations can achieve effective and sustainable compliance in 2026 and beyond.

Are you looking for pci dss compliance in UAE without complexity? You are at the right place. We at ValueMentor are a trusted cybersecurity partner that understands both PCI DSS requirements and UAE regulatory requirements.

FAQS

1. What is the first step to start PCI DSS compliance in the UAE?

The first step is to define the scope of your Cardholder Data Environment (CDE)-identify where card data is stored, processed, or transmitted. This helps focus your compliance efforts and reduce unnecessary complexity.

2. Do small fintech startups in the UAE need full PCI DSS certification?

Not always. Based on transaction volume, smaller fintechs may qualify for simplified validation methods like Self-Assessment Questionnaires (SAQs). However, they must still meet the core requirements of PCI DSS.

3. How often do UAE organizations need to renew PCI DSS compliance?

PCI DSS compliance must be validated annually. In addition, organizations are required to perform quarterly vulnerability scans and maintain continuous monitoring throughout the year.

4. What is a Self-Assessment Questionnaire (SAQ)?

An SAQ is a simplified validation tool that allows eligible merchants and service providers to assess and confirm their compliance without undergoing a full audit.

5. What is a Report on Compliance (ROC)?

A Report on Compliance (ROC) is a detailed assessment report prepared by a Qualified Security Assessor (QSA). It confirms that an organization has fully implemented and is maintaining all applicable PCI DSS requirements. ROC is typically required for Level 1 organizations, or when mandated by acquiring banks or regulators.

6. How does PCI DSS impact cloud-based payment systems in the UAE?

Organizations using cloud environments must ensure their providers are PCI DSS compliant and clearly define shared responsibility models for security and compliance.

7. Are digital wallets and mobile payment apps subject to PCI DSS?

Yes. If digital wallets or mobile apps store, process, or transmit cardholder data, they fall under PCI DSS scope and must comply accordingly.

8. What are the most common PCI DSS audit findings in the UAE?

Some common gaps include:

1. Weak access controls

2. Lack of proper network segmentation

3. Incomplete logging and monitoring

4. Insufficient third-party/vendor risk management

9. How does PCI DSS support fraud prevention in UAE financial institutions?

By enforcing strong encryption, continuous monitoring, and strict access controls, PCI DSS significantly reduces the risk of data breaches and payment fraud.

10. Can PCI DSS compliance improve customer trust in the UAE market?

Absolutely. Demonstrating compliance shows a strong commitment to data security and regulatory alignment, which enhances credibility and builds customer confidence.

11. What internal teams are responsible for PCI DSS compliance?

PCI DSS compliance is a cross-functional effort, typically involving:

1. IT and Infrastructure teams

2. Cybersecurity teams

3. Risk and Compliance teams

4. Legal and Operations teams

This is usually led by Compliance Officers and CISOs to ensure organization-wide alignment.